Updated February 2026

Introduction: When the IRS Stops Asking and Starts Taking

You’re not alone if you’ve received a letter from the IRS. For many, the first IRS letter feels manageable. But by the time their wages are garnished or bank accounts frozen, panic sets in. The truth is, the IRS sends warning signs long before that—and if you know what to watch for, you can act before things spiral.

What Triggers IRS Collections

The IRS initiates collections when it believes you owe money, and you haven’t paid or responded. Here are some of the most common triggers:

- Unpaid taxes after filing a return

- Failure to respond to IRS notices

- Not filing one or more required tax returns

- Repeated noncompliance after previous contact

- Large unpaid balances that raise red flags

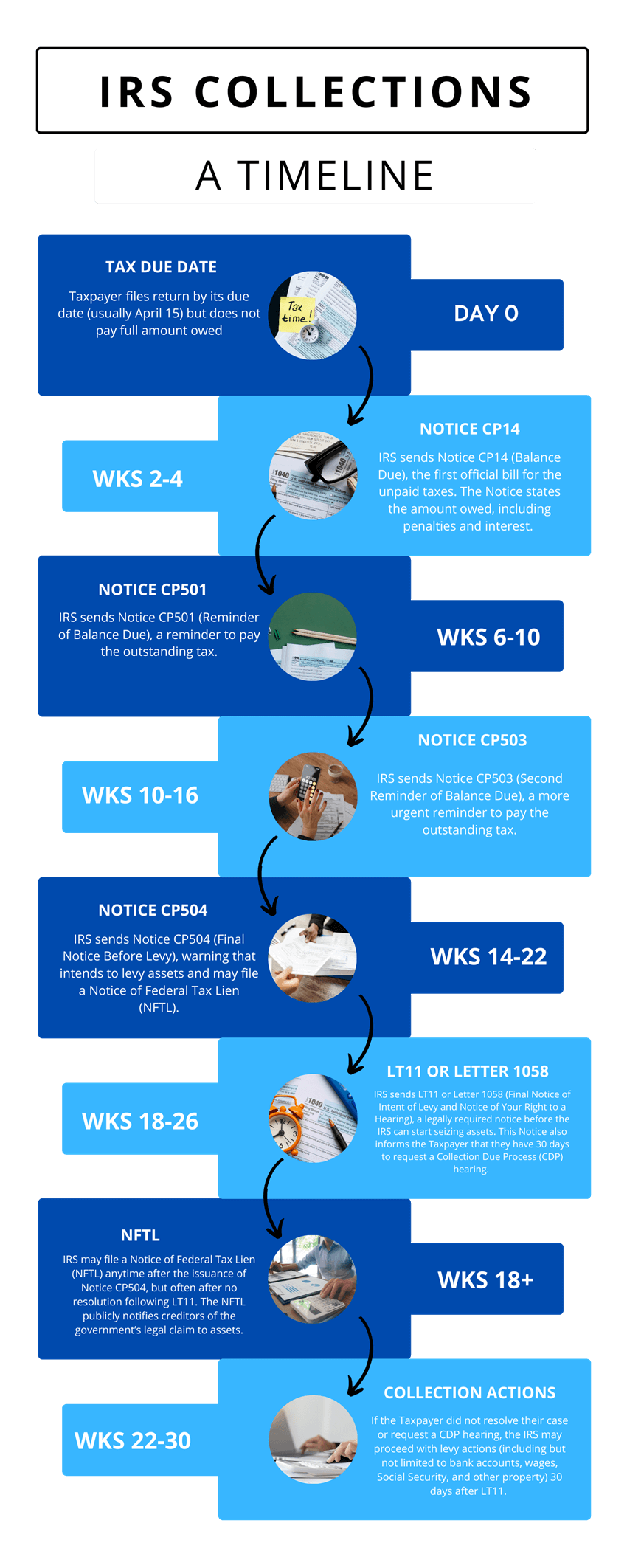

Before the IRS can collect a tax debt, it assesses how much you owe and officially records the tax liability in its system. How the IRS handles a $25,000 liability is different from how they handle a $10,000 tax debt Once this happens, the IRS usually sends a Notice of Balance Due (CP14) informing you of the amount due.

The IRS must notify you within 60 days of the assessment, and it has 10 years to collect the tax debt. If you ignore the first notice, the IRS will send additional reminders.

IRS Notices and the Collections Timeline

IRS collections usually begin with a series of mailed notices. Each one is a step closer to enforcement. Understanding what these notices mean—and where they fall in the timeline—can make the difference between fixing the issue and facing garnishment.

Typical IRS notice sequence: CP14 → CP501 → CP503 → CP504 → LT11 or CP90

Early Notices

These are initial contacts that notify you of a balance owed.

- CP14: Balance Due Notice – This is the first notice you’ll get if you owe taxes. It tells you the amount due and gives a deadline for payment before penalties increase. This notice starts the collection timeline.

- CP501: Reminder Notice – If you do not respond to CP14 by paying the amount owed.

- CP503: Second Reminder Notice – Follow-up urging action before the IRS takes further steps.

Final Notices Before Enforcement

These notices are more serious. Ignoring them may result in seizures or wage garnishments.

- CP504: Final Notice of Intent to Levy – Final reminder and severe warning that the IRS may start seizing your assets, such as wages or bank accounts, if you don’t act quickly. If you’re a business owner who has fallen behind, you may receive a CP504B.

- CP90, LT11 or LT1058: Final Notice of Intent to Levy and Right to a Hearing – Your last chance to prevent enforced collection actions. You have the right to request a hearing within 30 days. If you still haven’t responded, this notice informs you that the IRS may seize state tax refunds, wages, Social Security income, or other assets. This notice is especially critical because it explains your rights before the IRS takes further action. If you receive this notice, it is time to seek the guidance of a professional.

Other Notices

You may also receive reminders depending on your account status.

- CP71: Annual Balance Due Reminder Notice – If you are currently on an Installment Agreement or in Currently Not Collectible status (explained below), the IRS will send this notice each year to remind you of the amount of any unpaid taxes, including penalties and interest for a specific tax year.

How do I know what letter or notice I received?

If you received a notice from the IRS, look at the top right corner of the letter. Most IRS notices have a notice or letter number, such as CP14 or LT11, in the upper right-hand corner.

What the IRS Can Do If You Don’t Respond

Ignoring IRS letters doesn’t make the problem go away. It allows the government to take control of your income, bank account, or even your home.

The IRS can:

- File a federal tax lien, which is public and impacts your credit

- Garnish your wages directly through your employer

- Freeze your bank account and remove funds (a levy)

- Seize physical property (e.g., real estate, vehicles, business assets) in rare cases

We’ll explain each of these actions in upcoming posts.

What You Can Do to Stop or Reduce IRS Collections

You have options, even if the IRS has started contacting you. Some of the most common include:

Payment Plan (Installment Agreement)

Monthly payment plans based on your ability to pay. The easiest (and most common) option, which you can set up online if you meet specific requirements.

Currently Not Collectible (CNC) Status

Temporary pause on collections until your financial situation improves. However, it’s more labor-intensive than an installment agreement.

Depending on your financial situation and the amount of tax owed, some substantiation may be required in the form of bank account statements, bills/invoices, etc.

You’ll also face additional requirements to maintain CNC status.

Penalty Abatement Request

The IRS charges large penalties if you do not file or pay your taxes on time. Sometimes they will waive penalties automatically or upon request, depending on the taxpayer’s history of compliance and the reason for the late filing or payment. Common reasons include serious illness, natural disasters, or errors made by your tax professional.

This resolution must be paired with an installment agreement or other resolution, as the IRS will expect to be paid for the remaining balance.

Offer in Compromise (OIC)

Settle your debt for less than the full amount by proving that paying off the debt would create a financial hardship.

You must meet specific requirements to qualify.

The most labor-intensive. It requires you to compile lots of paperwork (financial statements and substantiating documents).

Collection Due Process (CDP) Hearing

Legal right to appeal before the enforcement of a Final Notice of Intent to Levy (CP504) or after a Notice of Federal Tax Lien (CP90) is issued. You can dispute your tax liability if you believe it is incorrect or propose an alternative resolution.

You can involve a separate party (the Independent Office of Appeals, separate from regular IRS Collections).

Also, it temporarily stops the IRS from garnishing wages, levying bank accounts, or seizing property if it has begun to do so.

However, you only have a limited window to request a CDP hearing; you must request it within 30 days of the date on an LT11/Letter 1058 or within 30 days of filing the Notice of Federal Tax Lien (NFTL).

We’ll walk through these strategies in more depth later in this series.

Know Your Rights

You have rights in the collections process. The IRS must follow strict guidelines, including:

- Providing written notice before taking collection actions.

- The right to dispute tax assessments and collection actions.

- Offering payment options and hardship relief to qualifying individuals.

- The right to seek assistance from tax professionals or legal representatives.

Why Timing Matters More Than Anything

The sooner you respond to the IRS, the more control you have over the outcome. Many taxpayers wait until it’s too late, when the IRS has already started garnishing wages or issuing levies. Don’t wait for the IRS to take control of your finances.

If you owe the IRS, look into your options and take action. Whether setting up a payment plan or getting professional help, there is always a way to move forward.

If you need help, consider talking to a tax expert who can guide you through the process. The sooner you act, the better your chances of resolving your IRS debt with the least stress possible.

Conclusion

IRS collections can feel like they come out of nowhere. But in reality, there’s a predictable series of steps leading up to enforcement. If you know what to watch for—and take action early—you can avoid the most painful consequences. In our next post, we’ll dive into IRS levies and how to stop them before they hit your bank account.

Owe money to the IRS?

Don’t wait until the IRS makes its next move. Schedule a confidential consultation with Wiggam Law today. We’ll help you understand where you stand, what’s coming next, and how to protect what matters most—your paycheck, your home, and your peace of mind..

FAQ: IRS Collections and Enforcement

How long does the IRS take to start collections?

Collections typically begin 30 days after a final notice (like LT11 or Letter 1058) has been sent and ignored. That timeline can shorten if you’re a repeat offender or owe a large balance.

Can the IRS garnish my wages without going to court?

Yes. The IRS is one of the few creditors that does not need a court order to garnish wages. Once proper notice has been sent and ignored, garnishments can begin.

What’s the difference between a lien and a levy?

A lien is a legal claim against your assets; a levy is the actual act of seizing them. Liens hurt your credit. Levies hurt your bank account.

Can I stop IRS collections once they’ve started?

In many cases, yes. Through legal mechanisms like installment agreements, Offers in Compromise, or Currently Not Collectible status, enforcement can be paused or reversed, especially with the help of a tax attorney.

What notice means the IRS is about to take action?

The most serious is the LT11 “Final Notice of Intent to Levy” or Letter 1058 “Notice of Your Right to a Hearing”. Ignoring them can lead directly to wage garnishment or a bank levy.